Capital Stack

Capital Stack is a term encountered mostly in commercial real estate projects, and it refers to the relative priorities of different lenders and equity holders in a property.

Capital Stack is a term encountered mostly in commercial real estate projects, and it refers to the relative priorities of different lenders and equity holders in a property. It’s often presented in a visual form to help investors understand their position in line relative to the rest of the financing. Somewhat confusingly, the further up the stack you are, the lower your priority is relative to those below you on the stack.

(The capital stack bears some similarity to a company’s “cap table”, which experienced angel or venture investors will recognize as the detailed formal record of a company’s ownership.)

Let’s start with the simplest example, which is a property you own 100% outright with no mortgage or debt. Assume you purchased a home for $100,000 in cash. In that case, the only party on the stack is you:

Most people don’t own real estate outright, they have a mortgage, and that mortgage is secured by a lien on the house. So if you don’t pay your bills, the lender has the right to take possession of the property and sell it off to recover the money they lent out. Assuming you had a standard bank mortgage on that same $100,000 property, with a 20% down payment, your capital stack would look like this:

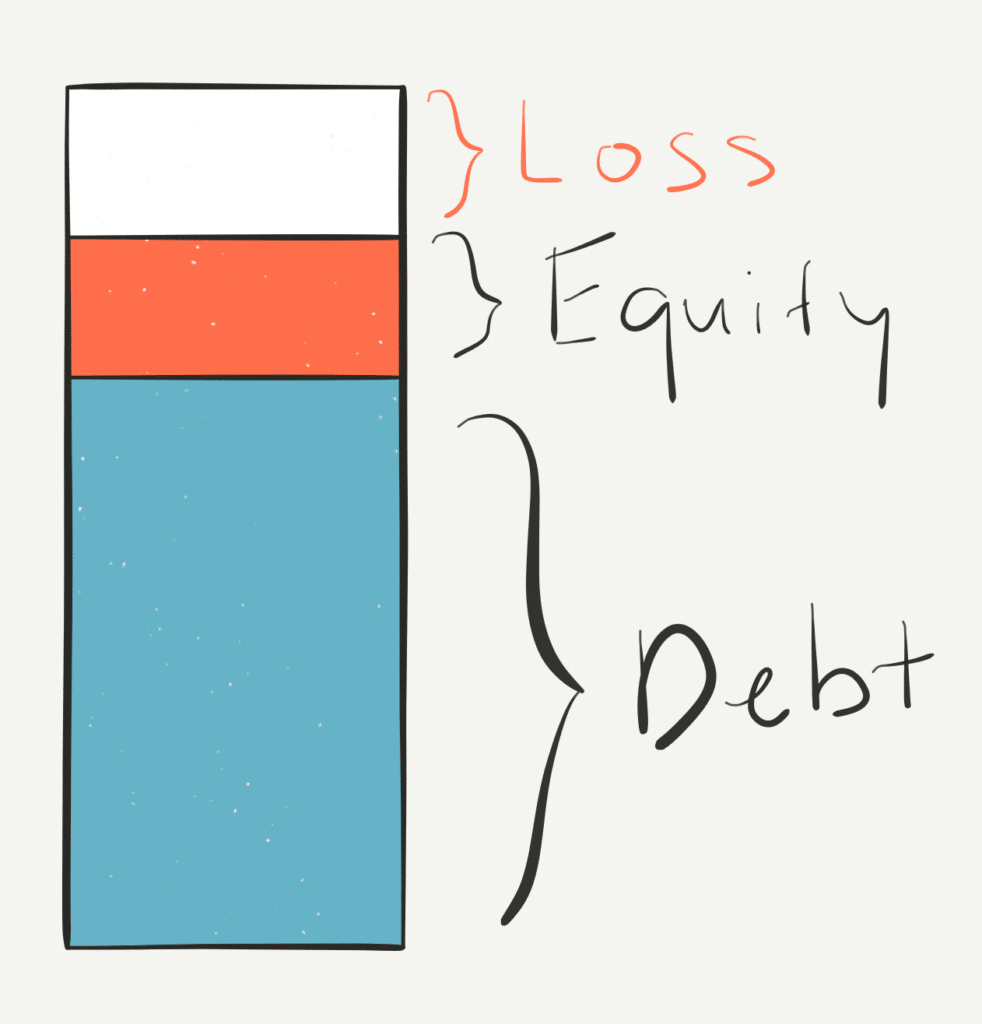

Now let’s assume that same house you bought for $100,000 is now worth only $90,000:

If the value of the property goes down, the amount owed to the bank doesn’t change, and they remain first in line to get paid if and when the home is sold.This is why most lenders will limit the maximum amount (often expressed as ARV or LTV) that they will loan on a property.

In this scenario, your equity of $20,000 has declined by 50%! On the flipside, if the home grows in value, the amount owed to bank also doesn’t change, and you get to keep all of the appreciation.

(A useful way to think about the capital stack is like a very tall glass. When an investment is “liquidated” and the glass is filled up, it fills from the bottom up toward the top.)

There’s nothing inherently good or bad about a particularly location on the capital stack, it simply corresponds to the level of risk (and therefore potential return) that each tier can expect from the investment.

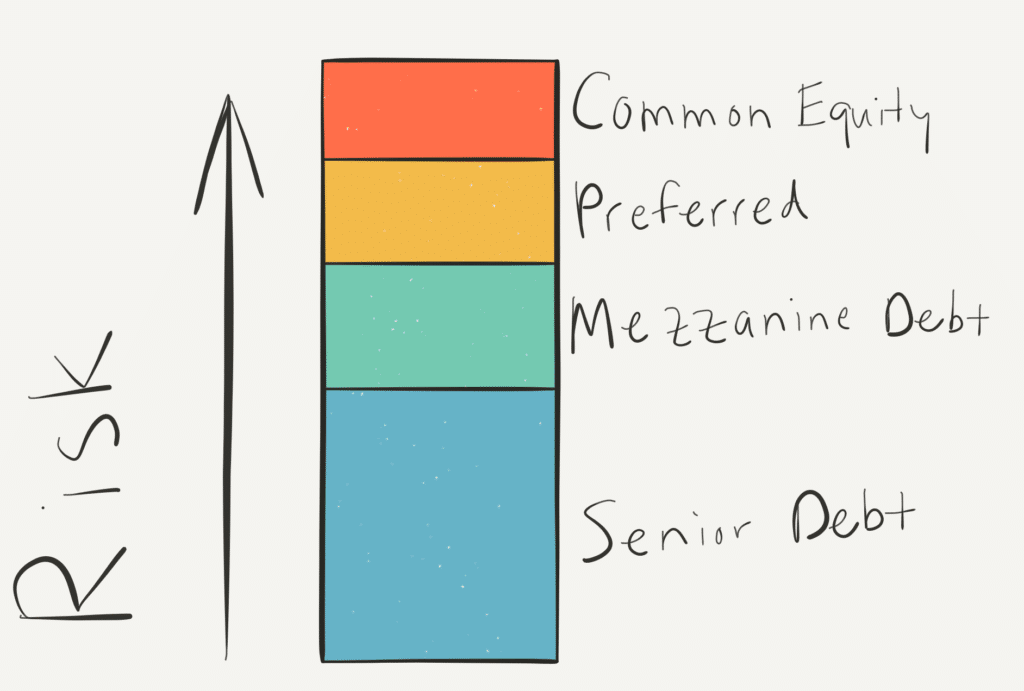

For example, in commercial real estate projects there may be more than one lender (kind of like a second mortgage on your house). That second lender will expect a higher interest rate on that loan because they know they’re taking a position behind someone else when it’s time to distribute the proceeds after the property is sold.

There are also variations on types of equity, with some classes of equity holders given preference (hence the term “preferred stock”) when distributing the proceeds. Here’s a simplified capital stack for a commercial real estate project:

(Following on the water metaphors of “liquidity” and “cash flow”, the actual implementation of the capital stack in terms of who gets paid how much and when is often referred to as the “waterfall”.)

Note that while risk increases as you move up the capital stack, so does the potential return. When reviewing crowdfunded real estate investments, an important part of due diligence is understanding the terms of the investment, including where you as an investor will sit in the capital stack. Again, there is no “good” or “bad” place to be, as long as you understand the potential return compared to the risk.

Want to learn more but aren’t sure where to start? You can explore 168 crowdfunding investment platforms in our database and learn more about the nuts and bolts of crowdfunding and alternative investing on our blog. Did you know you can use a self-directed retirement account to invest in many alternative investments? Rocket Dollar makes it easy, and when you sign up using that link you'll be helping to support YieldTalk.

Featured Reviews

EquityMultiple

EquityMultiple stands out among real estate crowdfunding investment platforms because their main investors and senior leadership come from institutional real estate finance, rather than being VC-funded. Seed funding for the company was provided by Mission Capital (later acquired by Marcus & Millichap) and their co-founders and board of advisors come from the New York real estate finance and law community. They offer fewer investments than some other platforms, but that’s a deliberate choice to take a more curatorial approach to dealflow. Overall, EquityMultiple is a solid choice for accredited investors looking for a hands-off way to invest in commercial real estate.

"Gain exclusive access to high-yield commercial real estate deals"

Read more

First National Realty Partners

First National Realty Partners (FNRP) is a commercial real estate private equity firm that focuses on grocery-anchored commercial shopping centers, offering both investments in individual properties and an Opportunity Fund across all of their offerings.

"First National Realty Partners (FNRP) is a rapidly growing commercial real estate private equity firm that owns and operates real estate throughout the United States. FNRP focuses on expanding its portfolio by acquiring market-dominant, well-located commercial assets well below replacement cost. "

Read more

Percent

Percent aggregates private-credit investments from a range of originators offering small-business, crypto, venture loans, litigation finance and more, including international debt investments. Low minimums.

"Percent unlocks exclusive private credit investments for your portfolio. Access select alternative investments on the platform powering the future of private markets."

Read more